Three leaders do the same core thing—help you get paid—but they were built for different jobs and stages. Here’s a plain-English guide to pick the right one for you.

Facts checked as of 13 Sep 2025.

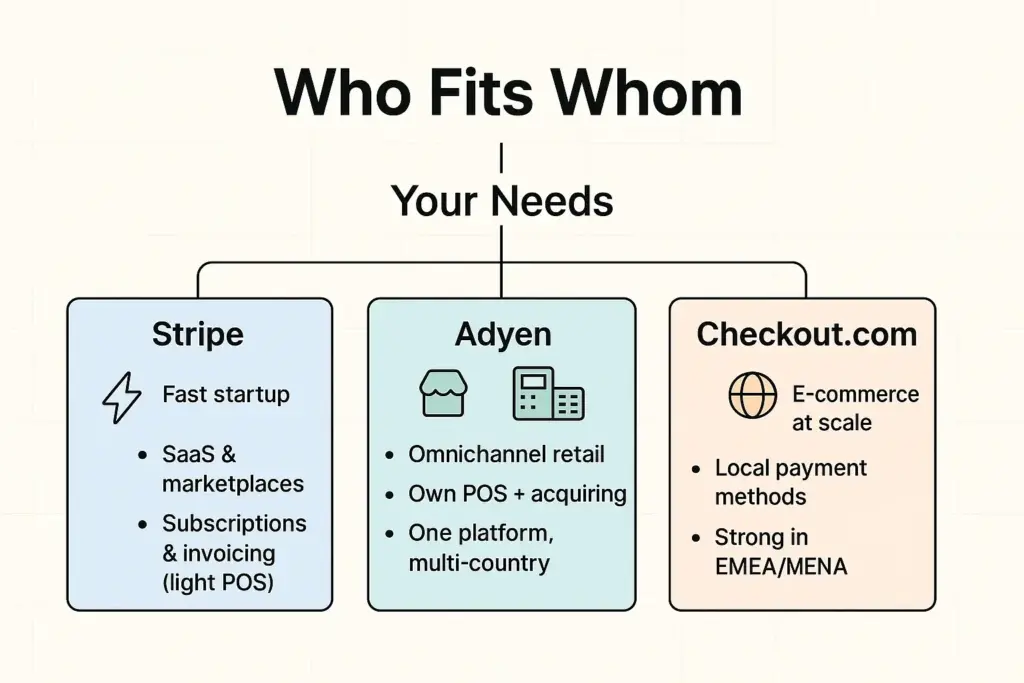

The short answer (cheat sheet)

- Stripe — best when you’re a startup, SaaS, or marketplace and want to go live fast with an “all-in-one” toolkit for online payments, subscriptions, and light POS.

- Adyen — best when you run a larger retail or omni-channel business in multiple countries and want one stack for online + in-store, with the company’s own POS terminals and bank-level services.

- Checkout.com — best when you’re a fast-growing e-commerce brand/marketplace with international sales and you care a lot about local payment methods (especially Europe and MENA) plus deep reporting.

How to think about the choice

1) Stage and business model

- Early stage / speedy launch. Stripe is the easiest lift: clean docs, quick onboarding, and ready-made modules (subscriptions, invoicing, payment links).

- Serious omni-channel. Adyen shines when you need one platform for web + app + physical stores across countries.

- International e-commerce with local methods. Checkout.com is strong where wallets, bank-to-bank, and country-specific schemes drive conversion.

2) Scale and hardware

- Mostly online (maybe some offline later). Stripe offers online first, with add-on Terminal and Tap to Pay if you need card-present.

- Heavy in-store traffic. Adyen has its own terminals and one back office for all markets and channels.

- Modular by flow. Checkout.com is often used as a flexible “build-to-fit” for marketplaces and APM-heavy checkouts.

3) Regulation and setup reality

- Adyen is a bank in the EU (Adyen Bank N.V.), which reduces middlemen and can simplify treasury and reconciliation.

- Stripe is not a bank; it works with licensed partners and focuses on developer-friendly products and platform tools.

- Checkout.com is a payments/EMI firm, not a bank; strong on compliance and market-by-market configuration.

Translation to plain English: with Adyen you can keep more of the payment chain “in-house.” With Stripe and Checkout.com you typically have partner banks under the hood—fine for most use cases, just structured differently.

4) Cards, wallets, and “local rails”

- If local methods (wallets, pay-by-bank, local card schemes) make or break your conversion, Adyen and Checkout.com tend to go very deep by region.

- Stripe supports many methods globally and gives polished, ready-to-drop-in checkout UIs; depth varies by market, so test on your target countries.

5) Issuing (your own cards)

- Stripe and Adyen both offer virtual/physical card issuing for expenses, payouts, and platforms.

- Checkout.com announced issuing in Europe/UK via partnerships in 2025 (with more markets subject to approvals), according to company statements.

Simple side-by-side

| Criterion | Stripe | Adyen | Checkout.com |

| Onboarding speed | Very fast, “out of the box” | Contracted, volume-based | Fast for online, modular setup |

| Online + in-store | Terminal & Tap to Pay | Strong own POS estate | Via partners/SDKs, case-by-case |

| Local payment methods | Broad coverage | Broad & deep | Very strong focus (EMEA/MENA) |

| Issuing (cards) | Available, multi-country | Available, enterprise | Announced for EU/UK (2025) |

| Regulatory stance | PSP, not a bank | EU bank + acquiring | EMI/PSP, not a bank |

Pricing without the pain

Don’t compare just the headline percent. For a real picture of cost and revenue, you should also look at:

- Authorization rates on your actual BINs and markets (this alone can outweigh a fee difference).

- Chargebacks and 3-D Secure logic (who absorbs what, and how smart the rules are).

- FX and cross-border add-ons.

- Wallets and device pays (Apple/Google Pay) specifics.

- Refund fees and operational overhead.

Pro tip: ask for an A/B pilot (one to two months) on your live traffic. Measure net captured revenue and dispute workload—not just fees.

Real-world fit: three quick scenarios

- You’re a SaaS with subscriptions in the US/EU. Start with Stripe: subscriptions, dunning, invoicing, plus POS if you need it later.

- You’re a retailer in six countries with web + stores. Look at Adyen: one stack for online and terminals, one set of reports, fewer moving parts.

- You’re a fashion marketplace expanding into MENA and Eastern Europe. Consider Checkout.com or Adyen if local wallets and bank-to-bank are critical—then proof it with an A/B on those markets.

What matters in 2025

Regulators keep raising the bar (for example, tougher safeguarding expectations for payment firms in the UK). Net effect for you: onboarding can feel stricter, but operational resilience is better. Treat it as a plus for customer funds and continuity, according to regulatory communications.

Bottom line

- Choose Stripe for speed, developer tools, and platform features.

- Choose Adyen for unified global acquiring and serious omni-channel with own POS.

- Choose Checkout.com for e-commerce and marketplaces where local methods and flexible configuration drive conversion.

Decision path: list your top countries, channels (web/app/store), need for issuing, and reporting needs → run an A/B pilot on your flows → pick the provider that wins on net captured revenue, not just on the sticker fee.

Want a concrete example of how local rails move the needle? Read our explainer: “UPI in India: How a Quiet Protocol Rewired Daily Money.”