India Stack ties together digital ID, paperless KYC, real-time payments, and consented data sharing. Built as open, API-first public rails, it helped India expand financial access fast, push onboarding costs down to cents, and set a model many countries are now exploring.

Why India Needed a Digital Infrastructure

Until the mid-2010s, India faced a double challenge: hundreds of millions of adults outside the banking system and public services slowed by paper and friction. The answer wasn’t a single app but a backbone — open rails that any licensed bank, fintech, or agency could plug into. That backbone became India Stack.

According to the World Bank, by 2021 account ownership had climbed to about four in five adults, up from roughly a third a decade earlier.

This vision materialized as a set of interoperable public APIs designed to bring identity, trust, and transactions into the digital age — and to put you in control of how your data moves.

What Makes Up India Stack?

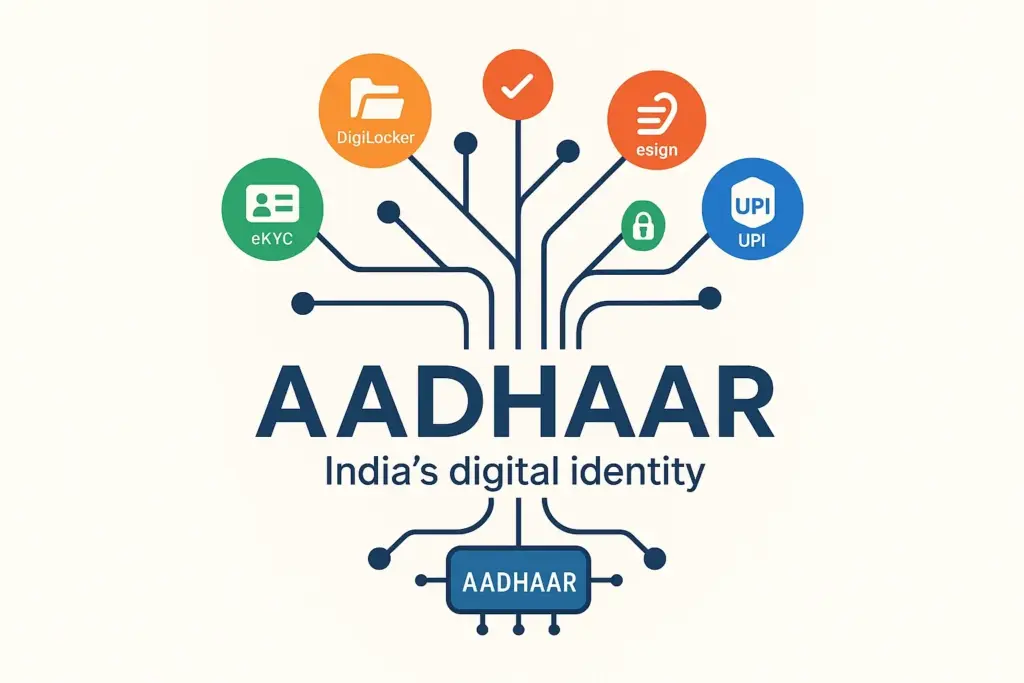

Identity layer — Aadhaar

India’s biometric digital ID underpins the stack. Today it covers well over a billion people, enabling universal, low-friction identity checks across banks, telecoms, and public services.

Paperless layer — eKYC, eSign, DigiLocker

You can verify yourself digitally in minutes. Policymakers and industry studies consistently show that moving KYC to standardized APIs and digital signatures drove costs from double-digit dollars to cents-level and cut onboarding times from weeks to a few taps.

Payments layer — UPI and beyond

Unified Payments Interface (UPI) makes instant, interoperable transfers possible — from QR scans at street stalls to enterprise payouts — so you can pay, get paid, and move money between banks without thinking about the plumbing.

Consent layer — DEPA / Account Aggregator

The Data Empowerment and Protection Architecture (DEPA) is India’s consent-based data-sharing model. In finance, the Account Aggregator framework lets you share verifiable financial data securely — only when you say so— to access credit, wealth tools, and more.

Together, these layers form digital public infrastructure (DPI) — publicly governed rails with open standards that the market builds on. As the IMF notes, this architecture fosters competition and inclusion while improving service delivery.

The Scale of Impact

- Inclusion. By 2021, about four in five adults in India had an account — a transformation in a single decade.

- Speed & cost. Digital KYC moved onboarding to minutes and pushed unit costs down to cents-level.

- Public spending. Government estimates point to double-digit billions of dollars in cumulative savings from direct, Aadhaar-enabled transfers that reduce leakages.

- Beyond finance. Open components first built in India were reused for verifiable health credentials during the pandemic, issuing billions of certificates across several countries.

Why It Works: The Open-API Playbook

Unlike monolithic government IT, India Stack was designed API-first. The state set common standards and governance; banks, fintechs, and platforms competed on UX and product. That blend — public rails, private innovation — is the engine. When the rules are clear and the rails are open, you get lower costs, faster iteration, and broader access.

Beyond India: From Pilots to Global Acceptance

- Cross-border rails. The UPI–PayNow link with Singapore expanded by mid-2025, widening participation and making low-cost remittances simpler for everyday users.

- On-the-ground acceptance. From the Gulf to Europe, acceptance partnerships are bringing familiar UPI checkout flows to Indian travelers and diaspora, starting with landmark locations and expanding merchant by merchant.

For developing economies, the idea is compelling: don’t copy Silicon Valley — adopt DPI tailored to local needs, with strong consent and privacy guardrails.

Mind the Caveats

Digital rails can exclude if last-mile access fails or if grievance redress is weak. Human-centred design, offline fallbacks (for example, Aadhaar offline e-KYC), and clear liability models remain critical. It’s important to keep balance: alongside big gains in inclusion and efficiency, researchers and reporters have documented cases where system failures created real-world frictions — so operational discipline matters as much as elegant standards.

Conclusion

India Stack showed how government can set the rules in digital finance: create open, safe standards — and let the market scale. If you’re a policymaker, entrepreneur, or investor, the lesson is simple: build interoperable, evolvable rails and let the ecosystem grow on top.

👉 Want to dive deeper into India’s fintech journey? Stay tuned to our blog — next we’ll explore how UPI turned India into a global payments leader.