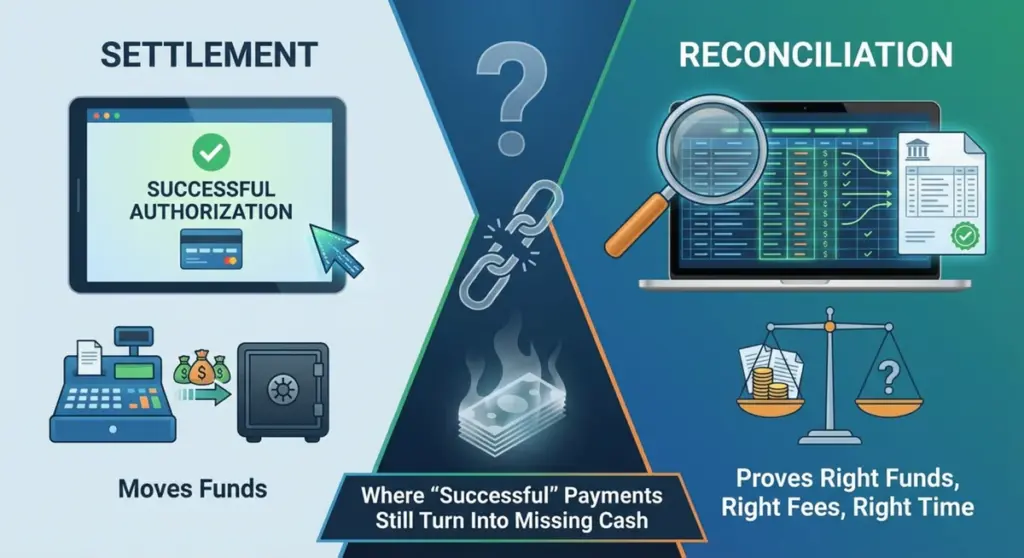

The checkout message tells you the authorization worked. It doesn’t tell you where the money is.

Settlement moves funds. Reconciliation proves the right funds arrived, with the right fees, at the right time.

The moment everyone stops looking is where problems start

A customer taps a card. Your app logs a conversion. The terminal prints a receipt.

That “success” is usually authorization: the issuer agrees the funds can be taken. It’s a promise with conditions, not cash in your account. The gap between “approved” and “funds arrived” is where the mess shows up later as:

- payouts that don’t match yesterday’s sales,

- fees that don’t align with your rate card,

- refunds that look correct in a dashboard but never hit the bank,

- finance reports that need a spreadsheet to “make them work.”

If you operate at any scale, this is not a rare edge case. It’s Tuesday.

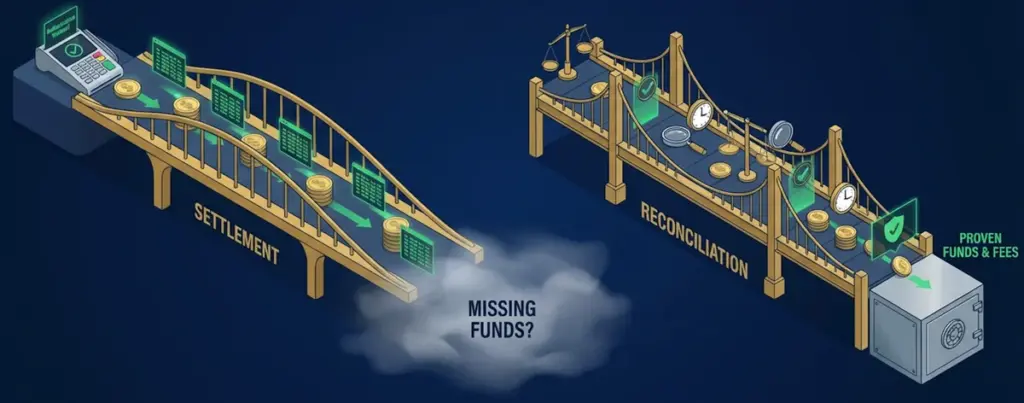

Settlement: the money-moving part (and why it’s not one clean event)

Settlement is the set of processes that moves money through the chain: acquirer → scheme/network → issuer → back to the merchant (via payout). It happens on schedules, often in batches, and it’s shaped by cutoffs, currencies, and adjustments.

Settlement is messy because it is:

- Time-based

Bank cutoffs, scheme windows, weekends/holidays, time zones, and batch cycles dictate when funds move. - Split into pieces

By scheme, region, currency, merchant entity, MID, outlet, or terminal. One business day can become multiple settlement files. - Adjusted along the way

Fees, reversals, chargebacks, and late-presented items show up after the “success” moment.

This is why the same “sales day” can produce multiple deposits, or why a deposit can cover several sales days.

Reconciliation: the proof layer (and why it can’t rescue bad inputs)

Reconciliation does not move money. It answers: Did the money that should have arrived actually arrive, and does every line item make sense?

It matches across different views of the same reality:

- your transaction logs (what you think happened),

- PSP/acquirer reporting (what they say happened),

- settlement files (what the networks processed),

- bank statements (what actually hit your account).

Reconciliation is where you discover:

- a subset of transactions never settled,

- a fee rule was applied differently than expected,

- a refund was accepted by the PSP but netted later (or not at all),

- identifiers don’t line up across systems.

If you want the mechanics of reconciliation itself (and why it’s a control system, not a “finance admin task”), read: Why Reconciliation Is the Hidden Engine of Payment Acceptance

Where money gets “lost” in real life

In most businesses, losses are not a single dramatic failure. They’re small mismatches that repeat.

1) Timing mismatches that look like missing revenue

Ops looks at daily approvals. Finance looks at deposits. If your payout cycle is T+2, and weekends shift value dates, the week’s numbers won’t “line up” day-by-day.

If you don’t explicitly model timing, teams waste hours arguing over which report is “right.”

2) Partial settlement and silent gaps

Some transactions authorize but never settle (or settle later) because of reversals, late presentment rules, or upstream breaks. If your monitoring ends at “approved,” you won’t see this until the bank statement doesn’t match.

3) Fee drift that shows up as margin compression

Fees are not just “a percent.” They are a stack:

- scheme/network fees,

- interchange components,

- acquirer/PSP pricing,

- currency conversion,

- additional services (tokenization, fraud tools, data products),

- adjustments (chargebacks, representment costs).

Even when every component is “valid,” the final net can surprise you if you don’t reconcile at the right granularity.

4) FX differences that make perfect reports look wrong

Authorization happens at one rate. Settlement can happen at another, and payouts can add another conversion layer depending on how your PSP structures it. Your “gross sales” can be accurate while your “net received” shifts.

5) Refunds and reversals that don’t behave like your product UI

Refunds are often asynchronous, netted, batched, or split from the original settlement flow. A “Refund successful” response is not proof the customer’s bank posted it, or that your net settlement reflects it as you expect.

Why finance finds the problem last

Because the truth is distributed:

- Product sees “orders paid.”

- Ops sees “transactions approved.”

- Payments sees “PSP reports.”

- Finance sees “bank deposits.”

If the identifiers don’t match across these layers, reconciliation becomes manual translation:

“PSP transaction ID ↔ order ID ↔ settlement reference ↔ bank narrative.”

That translation layer is where time disappears, and errors hide.

What payment teams do when they want fewer surprises

You don’t need a “perfect” system. You need a system that makes mismatches obvious early.

1) Make identifiers survive the full journey

Order ID, payment intent ID, PSP reference, acquirer reference, scheme trace, payout reference—pick a strategy so you can traverse from checkout to bank deposit without guesswork.

2) Reconcile at the right level, not just the top number

Daily totals are useful, but they’re where problems hide. The moment something is off, you need line-level matching: transaction → settlement line → payout line → bank line.

3) Treat settlement as an operational signal

Settlement isn’t only “finance stuff.” It tells you whether the system actually delivered what your checkout promised. If you care about cash flow, fees, and disputes, settlement data belongs in your operational dashboard.

The simple mental model

- Authorization: permission

- Settlement: money movement

- Reconciliation: proof

If you treat authorization as the finish line, you’ll keep discovering issues when it’s already expensive to fix them.